Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

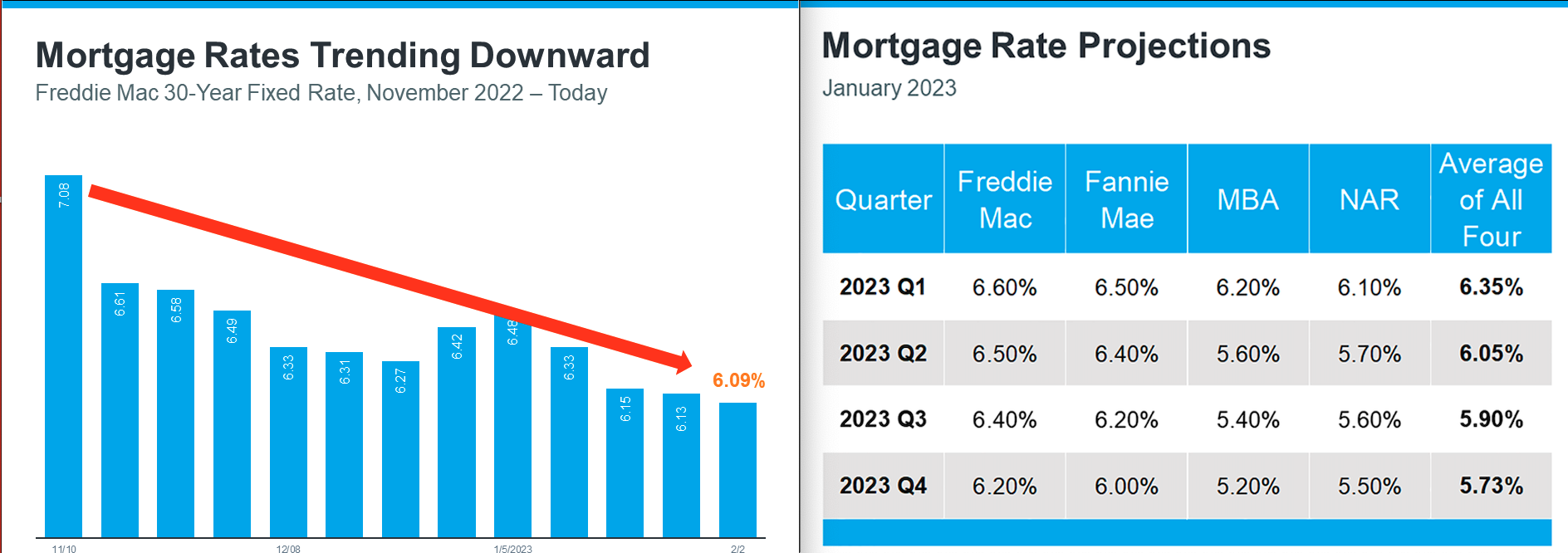

Interest rates have jumped from under 3% to close to 8% in the past 2 years. We’ve all heard about it, and it’s causing many would-be buyers to postpone their dreams of buying their first homes or making a move they had been considering. I’m here to tell you why that might not be the best strategy.

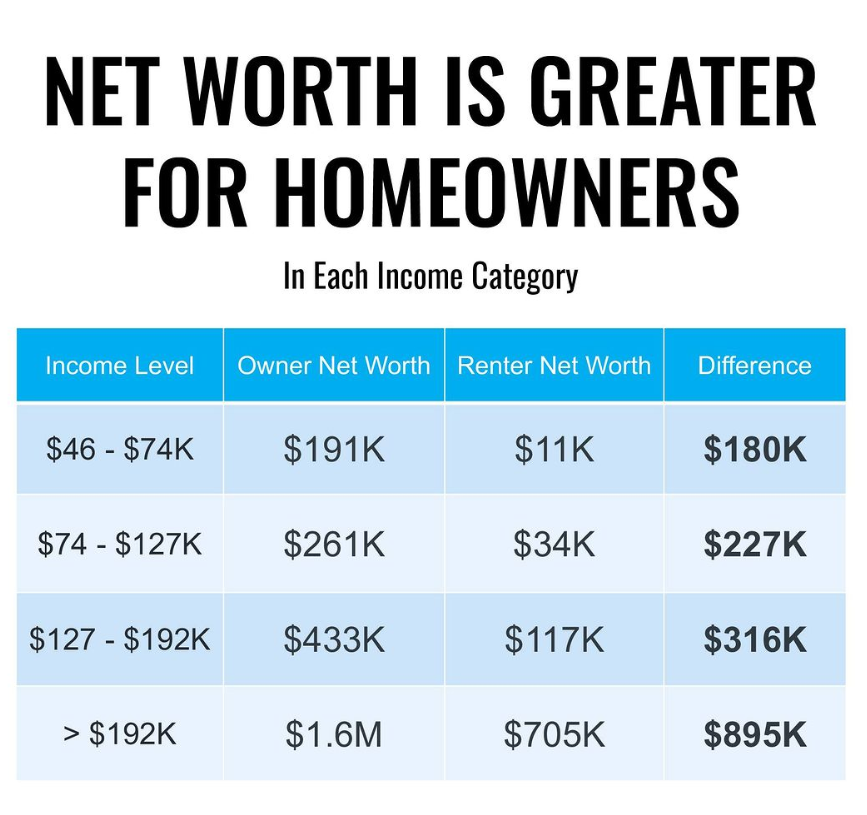

The real estate market is a diverse and ever-changing landscape, and different real estate markets offer a wide range of advantages and challenges, making them beneficial for varying types of buyers. Just because interest rates are higher now than they have been in several years, they are still low from an historical perspective, and, especially if you fall into one of these categories, buying now may still be a lucrative opportunity.

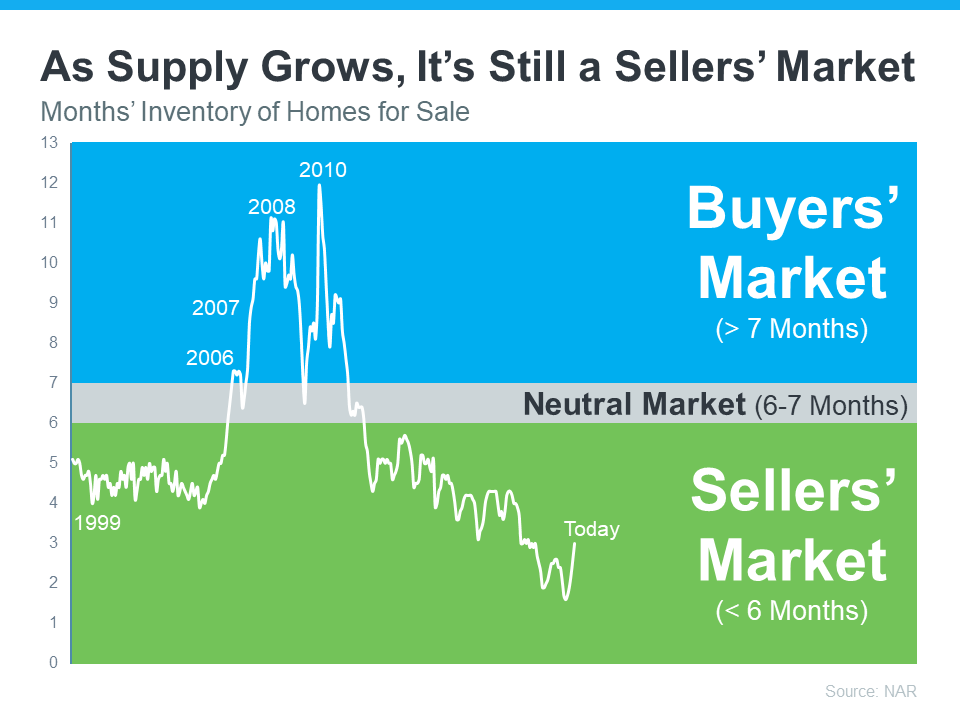

First Time Homebuyers. If you’re thinking of buying your first home, it could be a mistake to wait until rates are lower. When they do go down the market will likely be flooded with buyers who have been waiting. Given the low inventory levels of homes on the market, it could be tough competition again where buyers need to pay 10-20% more than the asking price and forego inspections to get an offer accepted. It might make sense to buy now, pay a more reasonable price, and have the benefit of a full inspection so you don’t get stuck with unexpected expenses and repairs. You’ can start to build equity through appreciation now and will still have the option to refinance when rates are lower.

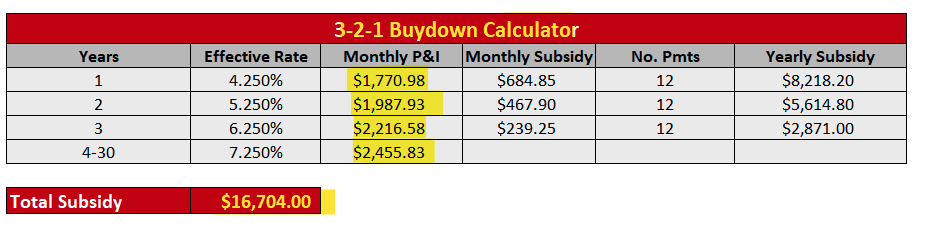

Downsizers. It’s a great time to sell. Prices have continued to increase, so you’ll be able to cash in on the equity from your current home and put that equity into your purchase. If you’re buying something less expensive than you are selling, the impact of the higher interest rates should be minimal because you’ll be borrowing less than first time homebuyers or people “buying up.” You can also consider utilizing a rate buydown to reduce your monthly payments and then refinance when rates are lower.

Investors. Yes, interest rates are higher, but so are rents. According to an article in the Herald Review, asking rents surged 4.6% year over year in the Midwest. With rents and home prices continuing to increase, you should think about taking advantage of the current market.

Cash Buyers. Last but certainly not least — If you are a cash buyer, what are you waiting for? Interest rates won’t affect your purchase or monthly expenses. The National Association of Realtors expects home prices to rise by 2.6% in 2024, so the longer you wait the more you will pay. In addition, buying now when rates are higher and fewer buyers are in the market, will mean less competition for prime properties.

The real estate market is not one-size-fits-all. Different markets cater to different buyer situations, needs, and investment strategies. It’s essential to understand the dynamics of our current market to make informed decisions and optimize your real estate experiences and outcomes. Let’s talk about what makes sense for you.